Subscribe to our newsletter to stay updated about the global markets.

ERShares XOVR Expands Access to High-Growth Private Companies and Sets a New Standard for Private Equity Valuation in ETFs

New York, NY – [2/26/28] – ERShares, the issuer of the XOVR ETF, the first exchange-traded fund to integrate private equity into its portfolio, continues to lead the financial industry with an innovative investment strategy. With a diversified portfolio that includes SpaceX (currently 10% of total holdings) and exposure to Klarna, a leading fintech company preparing for its IPO, ERShares is setting a new standard... for investor access to high-growth private companies.

Bridging the Gap Between Private and Public Markets

In a recent interview on Fox Business, Eva Ados, Chief Investment Strategist at ERShares, discussed the growing issue of private companies remaining private longer and limiting access for retail investors.

“As the IPO landscape evolves, many high-profile companies, including SpaceX, are delaying their public offerings. This limits access to only accredited and institutional investors, leaving retail investors out of some of the most significant wealth-creation events,” said Ados. “Some industry players prefer to keep private equity out of reach for retail investors, reinforcing a system where only institutional and accredited investors can benefit. At ERShares, we believe in democratizing access to these opportunities, ensuring that everyday investors can participate in the growth of tomorrow’s industry leaders before they go public.”

A New Era of Private-Public Investing

Opportunities for investors to access high-potential ventures at IPO valuations of around $560 million—similar to Amazon in 1997 or Nvidia in 1999—have become increasingly rare or even nonexistent in today’s markets.

“With private companies delaying IPOs, retail investors face increasing barriers to these high-growth opportunities. Our fund is designed to bridge this gap, providing investors access to promising companies like SpaceX, along with exposure to companies such as Klarna, before they reach public markets,” said Dr. Joel Shulman, Founder and CEO of ERShares.

Enhancing Private Equity Valuation Standards in ETFs

ERShares remains committed to adhering to industry best practices in valuation methodologies for private equity investments held within ETFs. XOVR’s pricing framework follows structured, research-backed principles to ensure consistency and transparency in valuation practices.

“Valuing private equity within an ETF requires a rigorous, multi-factor approach that accounts for market-driven price discovery mechanisms,” Dr. Shulman explained. “We adjust valuations based on tender offers, IPOs, ERShares’ private transactions at new price levels, and significant market movements with volume and activity. Our team continuously monitors these holdings using diverse, verified data sources to ensure our net asset value (NAV) accurately reflects real market dynamics while maintaining compliance with industry valuation standards.”

ERShares continues to lead in private market investing and ETF management, providing investors with access to high-growth companies before they go public. Acknowledging the evolving landscape of private market data, the firm remains open to refining its valuation methodologies as more reliable real-time pricing emerges.

The Future of Investing: Expanding Access to Private and Public Markets

As ERShares continues to expand access to pre-IPO investments, it remains committed to providing investors with exposure to high-growth companies through a disciplined and research-driven investment approach.

“We continue to provide evidence of how this private-public model works,” added Dr. Shulman. “Our approach will soon become clear as upcoming IPOs unfold, reinforcing the value of integrating high-growth private firms into a diversified portfolio. The future of investing is no longer just public or private—it is both.”

Past performance is no guarantee of future results, please refer to the disclosures below: https://entrepreneurshares.com/disclosures/

Big tech stocks have notched big gains, but they still have room to move even higher throughout May and the rest of 2021, said Joel Shulman, founder and CIO of ERShares, in an interview with Fox Business.

Despite setbacks for some major companies, selected FAANGS are performing strongly thus far, said Shulman. “It’s unbelievable, these companies [Facebook (FB)Amazon (AMZN) and Google (GOOGL)] are $4.5 trillion and yet they’re still growing 40-50%.”

All three companies have pivoted to perform exceedingly well in the midst of the pandemic, he pointed out, with Amazon’s EBIT increasing by 36%: “we haven’t seen this type of company ever.”

While many companies outperformed expectations, Shulman believes that some value stocks or high fliers “may be in trouble,” as exemplified by Twitter (TWTR) last week and Pinterest (PINS).

Changes in the capital gains tax could also introduce some “choppiness” into the markets, he said.

Earnings Season Takeaways

First quarter reporting saw 95% of tech stocks beating earnings, noted Shulman, but their recent volatility has made it difficult for analysts to predict what to expect next.

Analysts are “having an extremely hard time” predicting the trajectory of even well-known companies like the FAANGS, where predictions were way off. Avis Car Rental (CAR) is a value stock that personifies this; it is currently at an all-time high after being close to bankruptcy a few months ago.

“Unfortunately, with earnings so far, the guidance hasn’t been very helpful,” he added.

Individual Investors Holding More Stock Than Ever

New reports indicate that individual investors are holding more stock than ever; in April alone, stock holdings comprised 41% of total financial assets for U.S. households.

Individual investors’ money will “help fuel the markets” and encourage growth, argued Shulman,

“We saw what happened last year,” he said, noting that individual investors opened up accounts with Robinhood, Schwab, and IBKR en masse. But “there’s still a lot of cash on the sidelines.”

Individual investors are putting their money into Coinbase and Bitcoin, as well as high growth stocks, which have taken a hit recently.

Consequences of the Higher Capital Gains Rate

When asked if he was worried about the Biden administration potentially gearing up to push higher taxes, Shulman acknowledged that corporations and entrepreneurs could encounter more issues.

“As we’ve seen in the past, when corporate rates go up, it encourages companies to go offshore,” he said.

That’s because increasing capital gains taxes encourages companies and entrepreneurs to find ways to cut taxes, either through avoidance or evasion.

Specifically speaking to the entrepreneurial sector, Shulman said that entrepreneurial growth could be inhibited, because as taxes increase, founders and CEOs are going to “scale back on some of their growth in the organization development” as well as “the R&D and the properly planning equipment expenditures they’ve been making.”

Overall, however, Shulman remains positive on the outlook for the rest of the year. “We think we’re going to end the year higher,” he concluded.

Though the markets currently possess several vulnerabilities, there remains plenty of potential for investors, said ERShares’s COO and chief investment strategist Eva Ados in an interview with TD Ameritrade.

“It’s a stock picker’s market right now,” she said. “There are opportunities in value, and there are opportunities in growth.”

In the current markets she recommends a selection of the FAANGS: specifically, Facebook (FB), Google (GOOGL), and Amazon (AMZN). These companies are the “best of both worlds” in terms of growth and value, and they have been able to capitalize on the switch to e-commerce because of the pandemic, said Ados.

They’re “behaving like a regular growth stock,” with modest P/E ratios and valuations coupled with extraordinary growth. Facebook reported 50% revenue growth with a P/E of 25, Google reported 30% revenue growth with a P/E of 28. Meanwhile, Amazon reported 45% revenue growth and an EBIT growth of 35%.

“You have extraordinary margin when it comes to Amazon, and all of these companies,” said Ados.

Few Earnings Surprises for Tech

Broadly speaking, the tech sector isn’t participating much in earnings winnings, because earnings were coming from such a high base already. “It’s really hard to see earnings surprises” right now, said Ados.

As a result, investors are chasing value stocks still offering tantalizing earnings, but Ados warns that the value factor is coming from a low base.

“The danger there,” she explains, “is that we are pushing them to frothy levels.”

These tech stocks may never reach the levels they were at before the pandemic because our behaviors have changed, putting their business models at risk of high debt leverage, drastically decreased revenues, and even bankruptcy.

“We don’t think that chasing value companies just on the basis of earnings surprises is the right thing to do right now,” she added.

Risks Persist in the Market

The market has swung from growth to value quickly, says Ados. Hyper growth tech peaked on February 20th; then in mid-March deep discount value peaked; and now the broader indexes have peaked, hitting all-time highs.

“As a result, now the system is very vulnerable to any shock,” she added. The risks in the short-term include new mutations of the coronavirus, and whether or not vaccinations will work on them.

Another concern is the behavior of the retail investor. The recent record influx of retail investors to platforms such as Robinhood has led to markedly increased investing around specific companies. Millennials tend use online forums and social media to communicate about their ideas “and as a result they crowd the same names,” explains Ados.

These investors have collectively pushed specific growth companies higher. The thing to watch for, she adds, is a potential mass exodus from these same companies, causing them to “drop significantly.”

Artificial intelligence (AI) isn’t just a standalone investment theme; it’s a technology that could potentially “expedite the automation and cost-saving of every industry” through a deep learning revolution, according to ERShares.

ERShares’s flagship fund, the ERShares Entrepreneurs ETF (ENTR), offers exposure to a range of disruptive technology sectors—including robotics and AI.

With its emphasis on high growth companies driven by strong leaders, ENTR offers access to several AI-driven stocks with an entrepreneurial twist.

Alphabet

For example, Alphabet (Nasdaq: GOOGL), has robust robotics and AI divisions working to integrate both technologies into everyday life.

Via TensorFlow, an open source end-to-end machine learning platform, Google has endeavored to make its own machine learning platforms accessible to both beginners and experts, as well as an extensive library and models for experimenting with, per the TensorFlow website.

In addition, Google’s Gradient Ventures, a venture fund that is AI-focused, targets early-stage tech start-ups. It utilizes Google’s experience as tech founders and entrepreneurs to help tech start-ups launch successfully. To date, Gradient Ventures has funded over 67 start-ups ranging across industries from fintech and insurtech, to healthcare and life sciences, per the Gradient Ventures website.

Though Alphabet is a massive company, it remains entrepreneurial in spirit, through consistent leadership by co-founders Larry Page and Sergey Brin, who remain board members and controlling shareholders, and by its commitment to support tech start-ups. Currently ENTR holds 7.09% of its portfolio in Alphabet.

NVIDIA

Another robotics and AI mainstay is computing hardware manufacturer NVIDIA (Nasdaq: NVDA), which was co-founded by current President and CEO Jen-Hsun “Jensen” Huang.

NVIDIA’s graphics cards power the machinery of everyday life, from computers to cell phones; the company makes powerful graphics processing unites (GPUs) dedicated to artificial intelligence and deep learning applications. The company has also developed a massive cloud-based software suite to bring artificial intelligence applications into enterprise settings.

ENTR holds 3.57% of its portfolio in NVIDIA.

FedEx

Finally…Fedex?

Yes, FedEx (NYSE: FDX), the delivery company, has integrated AI and robotics into every step of its delivery and sorting models.

Founded by current chairman and CEO Frederick Smith, FedEx has also partnered with several other companies to stay on the cutting edge of technology in its industry.

One such partnership is with Mercedes-Benz Vans to develop Coros, an AI package delivery tracking system. Coros, or Cargo Recognition and Organization System, is installed into the cargo space of the delivery vehicles and utilizes automatic barcode scanning and cameras to track packages in the cargo hold, giving real-time updates on their whereabouts. It also helps optimize sorting by using an LED system that indicates prime package placement.

FedEx Express has also partnered with Plus One and Yaskawa to install four robotic arms for sorting small packages and letters in its Memphis hub, per the FedEx website. This technology is among the first in its industry and is working to increasingly automate and enhance performance.

At ERShares, we position our firm to be a thought leader and have taken measurable actions to encourage companies we invest in to consider ESG angles. We realize that beyond the encouragement of particular ESG initiatives to the preceding companies, it is far more critical and impactful to bring awareness of the ESG issues at hand.

Bitcoin’s energy consumption and environmental impact now have extremely significant unintended consequences than mainstream stories suggest. Therefore, our team has worked to frame the issue and stand against Bitcoin as it uses a considerable amount of energy, the proportion of renewable energy utilized remains unclear, and regulations regarding cryptocurrency overall remain nebulous.

Bitcoin Mining Electricity Usage, Emissions Too High

Blockchain technology, although an incredible technological advancement, has astonishing and evident environmental footprints.

The energy consumption is rooted in the “crypto mining” that makes digital currencies energy-intensive as they are. Researchers estimate that “mining Bitcoin, the most popular blockchain-based currency, uses more electricity than entire countries like Argentina” (NY Times).

Although it makes up a small portion of the world’s total transactions, the carbon footprint involved compares to entire nations’ carbon footprints. Bitcoin energy emissions alone can further exacerbate global warming well beyond levels that can potentially lead to even more detrimental effects of climate change.

Gradually, the cryptocurrencies’ environmental impact is starting to vex climate policy. “If left unchecked, Bitcoin mining in China— where an estimated two-thirds of the world’s blockchain mining takes place—could make it difficult for the world’s largest polluter to meet its climate goals. China’s Inner Mongolia region said recently that it was moving to ban the practice because it was hampering the province’s efforts to meet the new carbon-emissions goals set by the national government” (NY Times). Hence, governments worldwide are beginning to crack down on crypto mining and lock in new climate change policies.

ERShares’s Stance On Bitcoin

ERShares has set its own standards by upholding a clear policy not to invest in Bitcoin for this very reason. In extension to this, most of our employees have adopted this policy for their personal portfolios for the same reason.

Our team also spreads awareness to the public through our media streams. For instance, Coinbase (COIN) made history as the first major cryptocurrency company to list its shares on a stock exchange in the United States, pushing its valuation close to $100 billion. (NY Times) Although hailed as a landmark moment for global digital currencies, we have also addressed the stock’s negative impact on the environmental and regulatory issues on the rise since its recent debut.

Within the financial industry, digital currency’s energy consumption can be overlooked as trivial compared to the implications of traditional banking. Therefore, we work to ensure that investors are more conscious of the Bitcoin system and its indirect effect on ESG.

There are efforts to make cryptocurrency technology more environmentally sustainable. Still, until they are enacted, ERShares will continue to oppose Bitcoin and bring awareness as a thought leader within the global financial industry.

Entrepreneurs: “Conscious Of Long-Term Consequences”

Behind the companies we invest in are entrepreneurs who work as thought leaders, much aligned to our own team culture. These companies are created by entrepreneurs who identified pain points in their personal lives and continue to develop new solutions. Our academic research also goes back twenty years and demonstrates the consistent outperformance of competition due to entrepreneurs creating a unique culture. Overall, they are conscious of long-term consequences and harness their resources in a productive and allocative manner.

Beyond the fundamental issue of Bitcoin, entrepreneurs think about innovation differently and consider the potential negative implications of the innovation disruption. Thus, we firmly believe that the companies we invest in and present to our investors as opportunities work to incorporate the same level of awareness within their organizations as we do internally at ERShares.

In this paper, we analyze the wealth creation amongst the 50 wealthiest individuals in the world, eventually narrowing its focus to the ones that are both self-made and entrepreneurs. Since those who are self-made might not necessarily be entrepreneurs considering both are of vital importance. For example, Warren Buffet is both self-made and entrepreneurial, but not an entrepreneur by definition we have opted for and will expand on in this paper. Similarly, Steve Ballmer, the ex-CEO of Microsoft, is self-made but was essentially an employee of the company. He is the only “employee” amongst the top 50.

We begin the analysis of the scale, source, and characteristics of wealth today. We then go on to tackle the highly contested title of “self-made,” eventually recognizing the relativism of the term and settling for a scale to measure it, as opposed to the binary thinking generally employed; that is, “people either are or are not self-made,” which is untrue. Next, we analyze the ones that aren’t self-made, amongst whom there is a varying degree of success post-inheritance. Then, the paper analyses the Forbes billionaire index to identify the top 50 self-made entrepreneurs and share their notable characteristics and insights into their success. After this, we compare the wealth of the list members to a metric that underlines the scale of money being discussed – countries’ GDPs. Moving forward, the report analyzes not just the individual, but the organizational wealth generated by the diverse range of entrepreneurs using the market capitalization of their companies. Ratios are created to identify the entrepreneurs’ wealth for the other stakeholders in their companies and those who use their products. The report concludes by identifying entrepreneurship as the direct or indirect source of the wealth generated by most members of the top 50.

Identifying and Understanding the Wealthy:

Table A presents the top 50 wealthiest individuals as of November 27th, 2020 (all story and financial data were sourced from Forbes on this date) . Some of the most important highlights of the table are as follows:

.

The number of centi-billionaires continues to grow, from 2 in 2019 to 5 in 2020. The exclusive club consists of four technology entrepreneurs from the United States, supporting the fact that technology-entrepreneurship is the most explosive vehicle of wealth creation. The single outlier was LVMH boss Bernard Arnault, a French Citizen and in the luxury goods space. His power in France was recently put on display when he managed to get the French Government involved in Tiffany’s turbulent acquisition.

Nearly half the list is from the United States (23). China claims 11 spots; France and Japan are claiming three spots each; Germany and Hong Kong are claiming two spots each; and Spain, India, Austria, Italy, Canada, and Mexico are claiming one spot each. Notably, all three French nationals on the list generated/inherited their fortunes in the luxury cosmetics (Bettencourt – L’Oreal) and luxury goods (Arnault – LVMH and Pinault – Kering) industry, capitalizing on France’s historical designation as the global center of fashion.

66

The average age of the members of the list was 66. The youngest member was Facebook Founder and CEO Mark Zuckerberg (36), while the oldest spot was shared by both the Hong Kong billionaires on the list – CK Hutchinson’s Li Ka-Shing (92) and Henderson Land Development’s Lee Shau-kee (92). While the Asian billionaires’ wealth stems from traditional industries like ports and properties, their heirs are preparing to take over soon and displaying their business acumen via more modern and exciting bets through family-funded VC arms and SPACs. The most notable is Richard Li’s SPAC bet with Peter Thiel.

Together, the group controls an estimated $2.863, T, with the average member worth $57.26 B. This represents approximately 30% of the total 9.435 T owned by the 1.8% of the world’s 2,825 billionaires (2019 figures from Wealth-X’s 2020 Billionaire Census)

The wealthiest individual on the list was Amazon’s Founder and CEO, Jeff Bezos, at $186.5 B.

$26.9 B

Entry into the top 50 required a whopping net worth of $26.9 B. The lowest position is currently occupied by Giovanni Ferrero, the scion and executive chairman of his family’s namesake Ferrero Group, the confectionery giant behind hits such as Nutella, Kinder, and Tic-Tacs.

Problem: Who holds the “self-made” title and who doesn’t?

The term “self-made” has been the cause of much controversy over the last few years as its definition isn’t fixed. Most notably, when then 21-year-old Kylie Cosmetics founder Kylie Jenner was named the world’s youngest self-made billionaire in 2019. She threw the media into a frenzy over how someone that had capitalized on her family’s fame could ever be considered “self-made.” Another notest by assigning self-made scores – a scale from 1 to 10, which indicates the degree to which a person qualifies as self-made. A 10 means you’re entirely self-made, whereas a one means you inherited your wealth and did nothing to grow it. So, yes, turning an upper-middle-class upbringing and $250,000 into a $186 B fortune classifies you as self-made, with a score of 8. Kylie Jenner, who was discussed earlier, was given a 7. However, Georgable but less contested example is the world’s wealthiest individual, Jeff Bezos, who got his parents to invest approximately $250,000 in Amazon in 1995.

Solution: The Self-Made Score

In reality, the concept of being self-made is very relative. In truth, the concept of being self-made is very relative. This is best explained through Forbes’s explains this be Soros “who survived the Nazi occupation of Budapest, fled Hungary under Communist rule and worked his way through the London School of Economics as a railway porter and a waiter,” is a perfect ten on the scale. Interestingly, Soros is worth $8.3 B today but would have made the top 50 list had he not donated $32 B to the Open Society Foundations.

On the other hand, Charles Koch ($44.9 B), the Chairman and CEO of Koch Industries (a company he inherited from his father), received a score of 5, indicating that he was involved in growing his wealth but isn’t self-made by any stretch of the imagination. Comparatively, Julia Koch ($44.9 B), the widow of Charles’ brother David, received a score of 1 as she had done little to grow her inherited wealth yet. The term “yet” is critical in the previous sentence as scores can change, provided the person goes on to generate wealth. Lukas Walton ($17.5 B), the grandson of Sam Walton (Walmart’s Founder), currently has a score of 1, but at the age of 34, he has his life ahead of him to change that.

Read more about the Forbes Self-Made Score (awarded to those on the Forbes 400) here.

An excerpt from the article above about the Forbes Self-Made Score reads as follows:

“The score ranges from 1 to 10, with 1 through 5 indicating someone who inherited some or all of his or her fortune; while 6 through 10 are for those who built their company or established a fortune on his or her own.”

In line with the statement above, to identify self-made, we looked for a score of 6 and higher. Since Forbes only awards a score to those in the US, identifying self-made US citizens was simple. For non-US members of the list, we identified Founders who didn’t inherit a sizable/identifiable fortune ($100M +) as self-made.

We see that amongthe top 50, 37 individuals are self-made, whereas 13 inherited their wealth.

The Non Self-Made Wealthiest Individuals

1 – Mukesh Ambani: The most exciting inclusion in the top 50 who isn’t self-made is Mukesh Ambani ($73.7 B), the wealthiest man in Asia, who is currently competing with Amazon’s Jeff Bezos for the digital market of the world’s largest democracy, India. Mukesh Ambani inherited half of Reliance, the conglomerate his father Dhirubhai Ambani founded, while his brother Anil Ambani took the other half. The fairness of the firm’s division is up for debate as the brothers’ fortunes, which once stood at approximately $40 B a-piece, have diverged to the point where Mukesh has nearly doubled his wealth, while his brother Anil is filing for bankruptcy. Mukesh Ambani is arguably the most successful of those who weren’t self-made, managing to diversify his fortune away from petrochemicals to retail and technology (via Jio, India’s largest technology venture). Today, he is essentially the gatekeeper of all meaningful foreign investments in India.

More about Ambani’s legendary mid-pandemic fundraise of $20 B for Jio here and here.

2 to 13 – Other Family Business Heirs: AfterAmbani, the wealthiest heir on the list is the heiress to the L’Oreal fortune, Francoise Bettencourt Meyers ($72.5 B). She is followed by three members of the Walton clan, who collectively form the world’s wealthiest family with a combined net worth of approximately (and ever-fluctuating) $215 B. After them come the two Kochs, the Albrecht siblings (heirs to the Aldi retail fortune), and David Thomson, the head of the media and publishing empire founded by his grandfather. The most notable holding in the Thomson clan’s portfolio is Thomson Reuters. Next, in the 42nd spot is Yang Huiyan, the heiress to Chinese real-estate firm Country Garden Holdings. She is closely trailed by two Mars fortune members, whose assets stem from success in the confectionery industry. Finally, the last spot on the list is occupied by a long-time industry rival of the Mars family, the Ferrero family’s head, Giovanni Ferrero.

The top 50 wealthiest self-made entrepreneurs were defined as the individuals who have created their wealth (not purely inherited) and categorized as entrepreneurs (identified as a founder of the source company or a significant contributor to launching a start-up idea). The following table, Table B, illustrates the top 50 wealthiest (self-made) entrepreneurs according to Forbes’ data as of November 27th, 2020, showing the net worth of each self-made entrepreneur to this date.

The worth of the top 50 self-made entrepreneurs combined is $2,255.6 B. Their average age is 55.8 years old. Approximately 68% of the top 50 individuals represent countries outside the United States. The top three geographic regions represented include the following: United States (32%), China (24%), and France and India (4%) each. The top 50 self-made entrepreneur billionaires are generally from the United States and made their money in the technology industry. Out of the top 50 individuals, only one is female – Wu Yajun, CEO of Longfor Properties. However, it is critical to note that below the top 50, there are relatively more women joining the self-made entrepreneur wealth creation path than ever before.

Most notably, the billionaires enjoy a high degree of achievement relating to innovative technology, including recent disruptive innovations such as cloud computing and e-commerce. All the top 10 self-made entrepreneur billionaires have brought innovation that binds their wealth creation success. Other achievements include getting welfare and employment despite the shift to advanced technology. For example, many companies, including Amazon, have hired more employees than ever during the world’s time of need during the pandemic that has left many jobless. They have also achieved great success in diversification and maintaining the wealth that they have created. Many of these self-made entrepreneurs continue to develop and adapt to innovations. They have also achieved the ability to work in a wide range of geographic regions while working under global regulations.

Certain controlled factors contributing to their success are their skills, expertise, and background in their fields before founding their successful businesses. This includes the ability to receive the appropriate education in the field to gain work experience that fits with their passion. A critical uncontrollable variable that has contributed to self-made entrepreneurs’ success is the ability to take risks and start a venture of their own.

Jeff Bezos is the founder and CEO of e-commerce Amazon since 1994. He started this out of his garage in Seattle. He currently holds the highest net worth in the world in real-time. He is also known for being the Washington Post owner and founder of the space exploration company Blue Origin. He always showed a great interest in how things work, such as transforming his parents’ garage into a laboratory as a child. His success runs from a diversified realm of business ventures, making him one of the world’s wealthiest. He began his education at Princeton University and afterward worked on Wall Street, later becoming the youngest Senior VP at D.E. Shaw investment firm. It was only a few years after that he decided to quit his job, and start his own online bookstore business, Amazon.com. He took a risk when he decided to leave his finance career at D.E. Shaw and get into the world of e-commerce. Bezos consistently created wealth through his diversification of Amazon’s offerings for users and major acquisitions such as Whole Foods grocery chain for $13.7 billion in cash. He has also worked to bring donations and help bring more jobs despite the vast innovations of e-commerce. During the current pandemic, Amazon hired approximately 175,000 additional employees.

Elon Musk is a South African-born American self-made entrepreneur who founded SpaceX and Tesla. He became a multimillionaire in his late 20s after selling his start-up company Zip2 to Compaq Computers. Elon Musk has worked to revolutionize the current innovation in history both on Earth and in space. Although he grew up with a family full of entrepreneurs that are now successful on their own, he created his own success at the time without enough money to provide for himself when he immigrated to Canada at age 17 and later to the US. Musk changed his plans considerably by deferring his attendance to Stanford and launching the first business venture, Zip2. He used the money he earned from sales, approximately $22 million, to found X.com merged with a company now known as PayPal.

Ortega began his career manufacturing textiles through a small family company in 1963. He is one of the top self-made retail entrepreneurs who launched the brand Zara in Spain. He has invested his dividends into real estate in many countries, including the major city-states in the United States. He highlights an exciting and innovative way to approach the retail reserve in Spain. He has always stayed away from the media for several years while working to amass a personal net worth of approximately $77 billion (as of November 27th, 2020 net worth). His unique success stands with his ability to upend the retail world aggressively and effectively by getting clothes on racks faster than anyone within the market, starting what is currently known as “fast fashion.” His self-made success begins with being born to a low-income family, due to which he had to leave school at the age of 14 to start making money. He is known for the continuation of innovation and believes that success is never guaranteed, so it is critical not to focus on innovating.

Eric Yuan is another notable wealth profile that has recently gained a tremendous amount of wealth through his company, Zoom Video Communications. He is the founder and CEO of this video conferencing company that heavily runs on cloud computing technologies. He saw success by starting with an idea while finding better ways to communicate with his friends and family. He helped build WebEx as VP before starting his own company, Zoom. He had the necessary skills and expertise in this industry before launching Zoom. His net worth moved 112% to approximately 7 billion dollars in the last three months of 2020 due to the current pandemic. He continues to incorporate new technologies and fix issues such as privacy and security issues immediately at hand before continuing to innovate its features. Zoom has demonstrated Yuan’s success by being a top cloud computing technology provider that began with an idea to address his own needs.

Understanding the Scale of Wealth Generated by the Self-Made Entrepreneurs:

To understand the scale of the assets generated by the top 50 self-made entrepreneurs, we compared their wealth and business impact to a scale that would force perspective – the IMF’s top 50 countries by GDP, from the United States ($20.8 T) to Peru ($195B). We compared these entrepreneurs and countries through four different methods.

If the top 50 entrepreneurs were a country, where would they rank in terms of GDP? The combined wealth of these top 50 entrepreneurs identified was $2,225 billion. This amount would rank as the 8th largest country by GDP– surpassing Italy’s tally of $1,848 and shy of France’s $2,551 billion.

How many countries’ GDP would the entrepreneur’s combined wealth equate to? It would take the nine nations with the lowest GDP on this list (of the top 50 countries) to edge past the combined wealth of these 50 billionaires. The combined GDP was $2,244 billion and included South Africa, Pakistan, Finland, Colombia, Romania, Chile, Czech Republic, Portugal, and Peru.

What percentage of their GDP do the entrepreneurs (grouped by origin) make up? These 50 entrepreneurs come from 15 different countries – 7 of which had only one representative. The only GDP comparisons of note are the US and China. The United States has the most entrepreneurs, with their 17 billionaires reaching a combined $1,099 billion relative to the country’s GDP of $20,807 billion or roughly 5% of the total. China has the second most with 13 entrepreneurs amassing $465 billion compared to the country’s GDP of $14,860 billion or 3% of the total.

Given that GDP is not the money made by a country but just the domestic product’s value, it is more akin to a company’s revenue. Hence, how do the revenues of some of the entrepreneurs’ companies compare to GDPs? Amazon’s revenue of $280 billion is just shy of South Africa’s 40th ranked GDP of $282 billion. Another intriguing comparison is between Google’s revenue of $162 billion and Kazakhstan’s GDP of $165 billion (which is not in the top 50 countries; it is 54th).

How Much Wealth (Personal and Organizational) has been Created by Top 20 Entrepreneurs?

To fully understand wealth creation, it is essential to recognize how much wealth is being created by these world-renowned entrepreneurs, including those they don’t make for themselves. From Table B, we can identify the Top 20 wealthiest entrepreneurs ranked by net worth. From American Jeff Bezos and his Amazon empire to Chinese He Xiangjian and his home appliance powerhouse, enormous wealth is being created in both personal and organizational means. For simplicity, we will define personal wealth as wealth that contributes to their net worth, and organizational wealth contributes to their company’s market capitalization.

The total net worth of the top 20 entrepreneurs adds up to $1.54 trillion. Over a third of this total is contributed by these five centi-billionaires: Jeff Bezos (Amazon), Bernard Arnault (LVMH), Elon Musk (Tesla), Bill Gates (Microsoft), and Mark Zuckerberg (Facebook). While the total net worth is an important indicator of these entrepreneurs’ wealth, it does not show the full picture. To see it, we need to take a look at the wealth that their companies are generating. Table C below shows the market capitalization of each of these top 20 entrepreneurs’ ventures. To keep this model simple, we are only including the primary entrepreneurial company associated with each person. In total, these entrepreneurs’ venture valuations amount to $19.55 trillion. This is almost 12 times the amount of wealth that these entrepreneurs have created for themselves.

Table C

Source

Market Cap ($B)

Amazon

$1,599

LVMH

$250

Tesla

$555

Microsoft

$1,627

Facebook

$791

Oracle

$174

Google

$1,210

Inditex

$108

Google

$1,210

Alibaba

$742

Nongfu Spring

$748

Tencent

$720

Bloomberg LP*

$60

Pinduoduo

$173

Nike

$211

Kering

$76

Rocket Companies

$45

Fast Retailing (Uniqlo)

$8,588

Dell Technologies

$52

Midea Group

$617

Table D

Name

Wealth Created for others ($B)

% Made for Them

% Made for Others

Jeff Bezos

$186

11.63%

88.37%

Bernard Arnault & family

$108

56.78%

43.22%

Elon Musk

$423

23.79%

76.21%

Bill Gates

$1,508

7.34%

92.66%

Mark Zuckerberg

$689

12.89%

87.11%

Larry Ellison

$95

45.37%

54.63%

Larry Page

$1,131

6.50%

93.50%

Amancio Ortega

$31

71.17%

28.83%

Sergey Brin

$1,134

6.32%

93.68%

Jack Ma

$679

8.46%

91.54%

Zhong Shanshan

$686

8.34%

91.66%

Ma Huateng

$663

7.93%

92.07%

Michael Bloomberg*

$5

91.50%

8.50%

Colin Zheng Huang

$122

29.45%

70.55%

Phil Knight & family

$160

24.01%

75.99%

François Pinault & family

$29

61.49%

38.51%

Daniel Gilbert

$2

95.11%

4.89%

Tadashi Yanai & family

$8,548

0.47%

99.53%

Michael Dell

$13

75.00%

25.00%

He Xiangjian

$580

5.92%

94.08%

*Bloomberg LP is a private company, and hence the values are estimates.

Taking a deeper dive into these numbers, we can subtract the $1.54 trillion that the entrepreneurs personally created to be left with a total of $18.01 trillion created for others by this group of entrepreneurs. Looking at Table D above, we can see the exact numbers of how much wealth has been created by each individual through their company for themselves and others. The column “Wealth Created” takes the market cap of each entrepreneur’s primary venture and subtracts out their net worth to see how much excess wealth is generated. An interesting feature of this data is that 12 of these 20 entrepreneurs have created over 75% of their company’s wealth for others. This serves as evidence that forming partnerships and finding good investors generates more wealth for everyone in the long run, as opposed to running a company alone (without partners or investors) to hoard the equity.

These entrepreneurs create not only personal and organizational wealth but also compound wealth. For example, Jeff Bezos’s Amazon enables others to sell on their platform, allowing them to generate wealth. Third-party sellers on Amazon contributed to more than half of the firm’s 2019 revenue at $280 billion. Another entrepreneur-built platform that is seen in this top 20 list is Facebook. Facebook, which owns Instagram, enables influencers to make a living through the marketing and sales and their sponsor’s products. By simply appreciating these platforms’ scale, we can see how they create wealth for their parent companies and founders and their users.

Conclusion:

Entrepreneurship is indeed the singule best vehicle for wealth creation, whether the wealth is directly or indirectly created. Among the list of the world’s 50 wealthiest individuals, 30 of them were entrepreneurs. However, we find that even those that weren’t entrepreneurs often have indirectly benefited from entrepreneurship; those from family businesses often have the entrepreneurial spirit of their previous generations to credit for their enormous wealth today; those who were investors tend to bet on entrepreneurial companies to generate value; those who were employees were led by entrepreneurs and encouraged to operate as start-ups do; even those who were divorced and widowed happened to be in the lives of those who had found wealth, directly or indirectly, from entrepreneurship.

The pursuit of entrepreneurship will continue to be the single greatest wealth creation source, enabling those with grit, drive, and other such characteristics to out-do any pre-existing wealth generated. To conclude, we would like to share an example of the previous statement: Today, the Waltons, who hold the title of the wealthiest family in the world (excluding monarchies and hyper-fragmented families), are worth $215 B. Jeff Bezos is worth $186.5 B. It is only a matter of time before he surpasses the collective Walton family, simply through wealth generation via the success brought by entrepreneurship ahead.

By Joel M Shulman Ph.D., CFA, ERShares Founder & CIO

Perhaps lost among investors in their mad dash to buy value stocks is the potential to bid up deep discount equities well beyond reasonable levels. While it is commonplace to bemoan the valuation of Tesla, which at 7X return in 2020 and an $800B market cap, would be on track to eclipse global GDP in less than 3 years. It is perhaps less commonplace to recognize over-exuberance among so-called value stocks. This may no longer be the case. Take for example a few of the neglected companies now approaching record price levels. This list includes well-known entities such as Marriott, Bloomin’ Brands (parent to Outback Steakhouse, Bonefish, etc.), and SeaWorld. Avis is also nearing a 15-year high and gets honorable mention for this list. Notwithstanding the compelling case that each of these companies deserve a healthy step up from pandemic bottoms, the height of current levels borders absurdity to even the most optimistic, rational investor.

Case in point. Marriott International, a longstanding beacon in the hotel industry, boasts a 94-year history, 7600 properties, and 30 hotel brands in 133 countries. Last year its revenues dipped 50%, coupled with plummeting margins, rising costs, skyrocketing debt levels, and other significant obligations coming due soon. If that weren’t crippling enough, heavily fortified, cash-bearing new entrants such as Airbnb, recently entered the arena with a disruptive approach that threatens the very underpinnings of the hotel industry. These new pioneers provide a variety of accommodations, without burden of capital investment, annual maintenance, or SGA infrastructure. This is almost identical to the case of Uber and Lyft who completely gutted the cab industry through disruptive technology. Moreover, as competitors feast on Marriott’s market share, the parent had to contend with a mountain of debt service arrangements, rising interest rates, and a never-ending supply of angry timeshare owners. Given these reasons it seems very perplexing to witness Marriott’s stock price anywhere close to an all time high level. Perhaps even more surprising than Marriott would be the examples of SeaWorld, Bloomin’ Brands, and Avis. In the past year, each of these companies has been flirting with bankruptcy, yet the first two rest at an all time high price.

SeaWorld Entertainment, still smarting from a 2013 film (Blackfish) and global campaign to boycott and shut down the enterprise, has experienced a catastrophic drop in attendance (81%) while fending off rumors speculating bankruptcy. An examination of the balance sheet suggests a healthy level of cash, but it belies the $2B of expensive debt recently raised (9.5% coupon) which was primarily used to cover past losses and resupply depleted working capital accounts. Recognizing that post-pandemic attendance will surely rise from the prior year’s debacle, it is still unclear how investors could price this stock to an all time high given longstanding neglect to property, plant, and equipment, and future debt hurdles. Bloomin’ Brands provides another puzzle to the over-priced “value” company situation. Parent to familiar brands such as Outback Steakhouse, Bonefish, and Carrabba’s Italian Grill, last year this company experienced significant drops in gross margins and revenues along with soaring debt levels. It has current lease and debt obligations that exceed short-term cash levels yet not unlike the other examples, this stock price has also recently reached the prized all time high accomplishment.

Each of these four examples undoubtedly warrants an increase from pandemic levels. However, it remains a mystery how investors can justify current all-time high price levels. In recent weeks we have witnessed high-flying tech companies fall, on average, 20-30% from market peaks, and in some cases as much as 50-60%. The latter appears to be a floor to the price drop. By contrast, strongly bid-up value stocks have the potential to drop much further. As Hertz, Sears, JCPenney, and other fallen angels have demonstrated quite clearly, the floor to an overvalued, debt-intensive company is not 50 or 60%, but rather 100%. Buyers beware. Price levels corresponding with Marriott, Bloomin’, Avis, SeaWorld, and other overpriced value stocks are vulnerable to a major correction without a chance for recovery. We maintain that investors need to be very careful in buying value stocks now. The value no longer exists in the traditional buckets contained within the Dow Jones and S&P 500. We maintain that it has reverted back to Tech. Prices are low, and we can see an extended rally for a few more weeks.

The US stimulus checks now commencing delivery, will generate confounding effects associated with countervailing forces. On the one hand a massive cash infusion piled on top of an already recovering economy will continue to stoke inflationary fears. Casualties to inflationary concerns include both bonds and equities, with the latter being punished for higher discount rates applied to distant cash flows. Offsetting market selling pressures associated with inflation (primarily by institutional investors), we are likely going to also experience a hearty infusion of retail (day traders) investors who will attempt to parlay their newfound largesse into a larger windfall. Past stimulus behavior provides a clear blueprint on retail buying behavior. Chief among their selections include a list of risky, (hyper growth) equity securities. And, investors who want to participate along with the herd can readily join popular investment chat boards and crowd into the same names (akin to Gamestop short squeeze, etc.). In the near term, we believe retail traders will triumph over institutional investors and help escalate equity prices. We realize that on any given day, potential selling pressures from nervous, interest sensitive institutional investors, can tip the balance toward massive reallocation. Regardless, retail investor flows will continue to exacerbate market volatility and focus on a relative handful of stock selections.

We believe the strongest gains will accrue to recently beat-up high flying growth stocks (including popular ADRs) with heavy concentrations in the Technology and Health Care sectors. Growth stock gains should dominate inflationary fears for much of next week, though interest rate spikes (especially among the price sensitive 10-year bond), could delay a tech recovery for an extended period of time.

The global economy has evolved considerably in the past century. Economic growth and productivity have witnessed a complete paradigm shift. Productivity fueled by industrial manufacturing, advancements in transportation, and innovations in oil drilling enabled developing nations to prosper and generate riches in steel, automobiles, airlines, and manufacturing facilities. Industrial Sectors built global titans such as Henry Ford, John D. Rockefeller, Cornelius Vanderbilt, and Andrew Carnegie. Much has changed since then. Today’s wealth creators no longer reside in Energy, Manufacturing, and other Industrial Sectors. Nowadays exceptional growth opportunities reside in Technology and Health Care and include Entrepreneurs such as Jack Dorsey, Jeff Bezos, Elon Musk, and recently departed Steve Jobs. And unlike the robber barons from past eras, they do not extract wealth from competitors through unethical practices or the breakup of unions. The new breed of Entrepreneurs creates wealth and jobs through capital markets that allow all stakeholders to share in the rewards as they grow. Moreover, today’s entrepreneurs lead by example and often have a loyal, sometimes fanatical fan base unlike tycoons from bygone eras who were universally loathed and lampooned.

The recent experience during the 2020 pandemic makes clear how much our global economy depends on nimble entrepreneurs who can pivot quickly and create wealth and jobs during uncertain times. Much of the wealth and job creation has occurred within the Health and Technology sector, and as we show below, has a heavy concentration among publicly traded entrepreneurial companies. Moreover, the growth in Health and Technology firms have strong ESG ramifications: virtually no environmental impact, provide major benefits to social growth and infrastructure development and are driven primarily by entrepreneurial leaders with strong governance traits. Given the well documented pattern of growth in the most recent periods, all signals suggest this trend will only strengthen in future years.

Clear Pattern in S&P 500 Composition–Technology and Health Care Sectors Gain Dominance

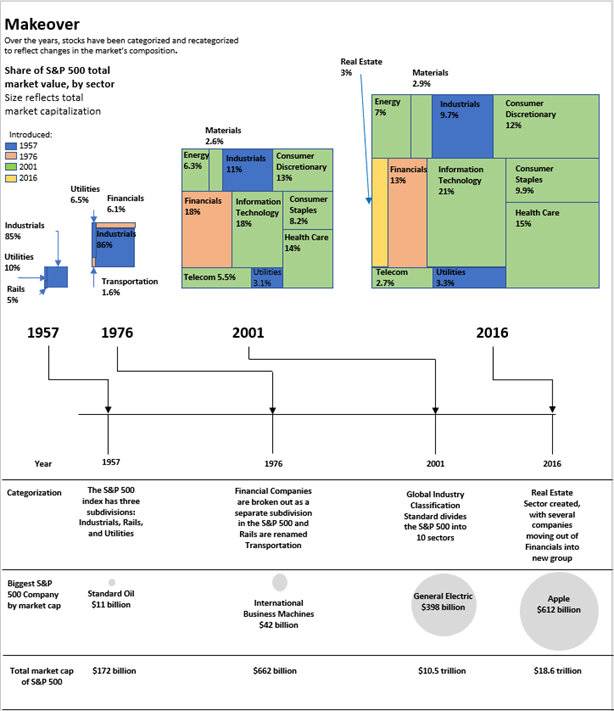

Early evidence of the Standard and Poor’s 500 Index (S&P 500) illustrates how even 60 years ago, Industrials comprised 85% of member constituents with Utilities and Rails holding 10% and 5% respectively (see exhibit below). Records from 1957 show how the S&P 500 total market cap was $172 billion with Standard Oil securing the top spot with a valuation of $11B. By 1976 the composition changed modestly with Industrials commanding (86%) of the total allocation, Financials (6%), Utilities (7%) and Transportation (2%). IBM was the heaviest market cap of $42B. In 2001 the S&P implemented a significant, more detailed classification makeover providing greater clarity in sector composition. General Electric ($398B) was the dominant firm in 2001 and the two main sectors were represented by Financials (18%) and Information Technology (18%) followed by Health Care (14%), Consumer Discretionary (13%), and Industrials (11%). By 2016, Apple ($600B) was the largest market cap company in existence, corresponding with Information Technology (21%) being the most significant sector. Other dominant sectors include Health Care (15%) and Financials (13%). In the approximately 60-year time of reporting, the S&P 500 grew total market cap from $172 billion to $18.6 trillion. Along with the substantial growth, however, the market composition changed considerably away from Industrials to Information Technology and Health Care.

In 2020, the S&P 500 composition shows Information Technology (27%) as the clear top sector with Apple ($2.1 trillion) as its most significant market capitalized firm. Health Care (14%) is the second most

significant sector followed by Communication Services (11%), Consumer Discretionary (11%), Financials (10%), and Industrials (9%). Notably, the concentration of the top 5 market cap weight stocks Apple ($2.1 trillion), Microsoft ($1.6 trillion), Amazon ($1.6 trillion), Alphabet ($1.1 trillion) and Facebook ($660 B) approximates half the total market cap of all 500 S&P constituents from just 19 years earlier.

Pandemic Accelerates Shift to Entrepreneurial IT and Health Care Companies by Order of Magnitude

Even prior to the COVID-19 health crisis in 2020, the trend toward Technology and Health Care was well established. However, the pandemic rapidly accelerated the timetable by a sizeable shift in magnitude. While the manufacturing, transportation, energy, and consumer discretionary sectors were essentially shut down, the Health Care and IT sectors, largely driven by entrepreneurial companies, immediately embraced the challenge to develop effective vaccines and immediate solutions to keep people safe and our economy running.

Work-from-home and virtual meetings, while developing in popularity prior to the health crisis, quickly became mandatory for economic survival. The health crisis fundamentally changed, overnight, long-standing habits and personal behaviors. In the absence of technological advances, individuals would not have been able to telecommute for work, enact virtual visits for business/personal conversations, utilize online shopping, complete ease of delivery or virtually visit with their health providers. Changes in behavior happened quickly, by necessity, and the health crisis expedited many work and personal changes that would have normally taken much longer to implement. It was Entrepreneurial Information Technology companies that primarily met consumer and business needs. Companies such as Zoom provide video technology for workers and students and other companies such as Amazon provide online shopping and ease of delivery. Netflix and Facebook provide entertainment and communication platforms to help fill additional personal needs. Notably, these companies represent only a handful of the many, entrepreneurial companies that quickly pivoted to meet market needs during a critical time period.

Importantly, Entrepreneurial Health Care companies like Moderna, Teladoc and Regeneron without hesitation promptly pivoted to build a new vaccine or breathing apparatus for victims desperately seeking a medical miracle. Other entrepreneurial companies enabled patients to virtually visit medical professionals in a timely, safe, efficient manner, without exposing parties to harmful disease. These entrepreneurs were the first to capitalize on an opportunity and propose workable, innovative solutions for the public. Not surprisingly, major Health Care companies were not actively visible in the early stages of the crisis. Traditionally, these companies miss timely opportunities and inaction due to sluggish corporate cultures steeped in corporate bureaucracy. Unprecedented circumstances disrupted conventional timetables. Health Care professionals and political leaders, who traditionally do not engage in active partnerships, fast-tracked processes and approval processes that were unthinkable until recently. Experimental drug tests have been discussed in real time, along with news updates concerning health and potential danger hot spots. All this new information can be attributed to innovative, entrepreneurial solutions.

Though the value of life, whether lost or saved, can be easily measured in the short-term with simple head counts, the true costs of the health crisis may require years to correctly assess. Fundamental changes in the way in which people live, work, commute and travel are likely. Further, individuals will likely change patterns in dining or entertainment venues (e.g., sporting events, theatre, etc.). Each of these changes have far-reaching ramifications on the quality and impact of life and influence the environment, social infrastructure and governance of our corporations and political establishments.

Health Care and Information Technology companies will continue to emerge as key contributors going forward. Health Care, in particular, will gain in prominence as life expectancy is expected to continue to climb.

Surging Life Expectancy Boosts Health Care Sector

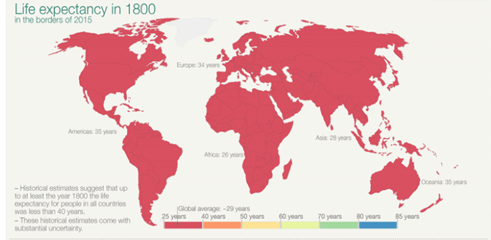

Arguably the strongest contribution any sector has made to mankind is within the Health Care sector. Although humans have inhabited the planet for well past 100,000 years, it has only been in the past 100 years that life expectancy has changed appreciably. Prior to the 1800s, regardless of location, human life expectancy was less than 40 years (see graph below). This longevity was true regardless of birth origin or economic prosperity.

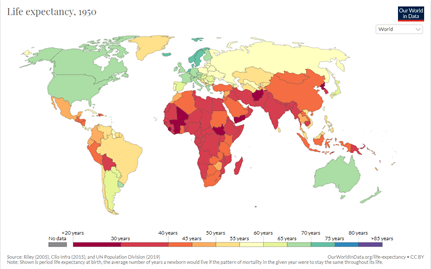

In the twentieth century, the gap began to widen considerably between developed and developing nations as modern health care emerged. Differences were substantial, corresponding with geographic location, and medical advances (see graph below). Those in developed nations, such as the United States, could expect a life of 70+ years whereas those in an emerging market would perish in approximately 1/2 that time. In some nations (primarily within Africa) average life expectancy fell below 30 years.

In recent years, the gap between developed and developing nations has narrowed with developing nations experiencing the strongest growth (see graph below). People residing in developed nations generally anticipate an average life above 80 years whereas those in developing nations rests closer to 65. Notably, life expectancy has virtually doubled in the past 200 years for all peoples with residents in developed countries receiving benefit in the 1800’s and developing nations seeing significant changes in the 1900s. Given the steady state in this important statistic for 99.95% of human existence, the recent medical advancements and pharmaceutical developments that have led to the doubling of life expectancy, in such a relatively short time period, represent a remarkable transformation.

Through these medical breakthroughs, individuals have been impacted in an unprecedented, positive manner. Humans now enjoy a longer, healthier presence with continuing enrichments delivered by the Health Care community on an ongoing basis, and it is this area that provides the most promise on a continuing basis. New research and innovations tracking early evidence of organ disease and malfunction, along with advancements in genomics (DNA), wearable technologies and artificial intelligence all will help extend the quality of life for humans. Many of the scientists behind these innovations are Entrepreneurs who drive much of the growth and through their companies we can monitor to gauge their representative journey through the Capital Markets. Although it is IT companies that dominate S&P 500 constituents, as we move to smaller capitalization area, it is Health Care companies that dominate, indicating the sector’s great potential for exponential growth in the near future.

Though 2020 has been a dismal year for most retail and travel company stocks, the same cannot be said for U.S. technology stocks such as Amazon, Tesla and Zoom Video. But how long will this growth trend continue?

All year long, stories have surfaced of global businesses that are thriving in an otherwise uncertain economy. These companies are showing exceptional growth and are, thus far, proving to be excellent investments. In just the past month alone, Non-U.S. equity ETFs have seen investments of over $25 Billion.

Based on these and other global trends, it is apparent that Non-U.S. Equities, especially Non-U.S. Small Cap funds, are outperforming U.S. equities across the board.

Here are three key ways that Non-U.S. Small Cap funds can outperform U.S. equities:

Intermarket Reversion

The time is right for an intermarket reversion. Over the past 50 years, U.S. Markets typically exceed Non-U.S. markets for periods of approximately 4-5 years before reverting, and then Non-U.S. markets dominate for a comparable period. We are now completing a period of 12-year dominance by U.S. Markets, which is about 2-3 times longer than the typical pattern. Moreover, during this period of 12 years, foreign stocks have significantly underperformed U.S. stocks. The Nasdaq 100 (QQQs) generated over 1000% (SP +400%) while the Shanghai Stock Exchange appreciated only less than 150%.

Tech Rout is Underway

In September, Tech stocks experienced a significant correction, with U.S. Large cap Tech dropping more than 10% in a single week. High-flying Tech stocks, such as Tesla, dropped even more. Though clearly some Tech stocks will continue to appreciate, it appears that the U.S. Tech sector as a whole is now fully priced.

P/E Relative Valuation

The price-to-earnings ratio of the Non-U.S. Small Caps at 15 is less than a third of the 47 P/E of U.S. small cap stocks. This provides further evidence that Non-U.S. Small Cap funds are currently better relative value.

So what does this all mean for you? How can investors capitalize on the opportunities created by these industries and companies around the world?

Diversifying your portfolio geographically through ETFs is a critical move that allows you to take full advantage of the current landscape. Now, more than ever, this opportunity is one that shouldn’t be passed up.

Why it is important to diversify geographically through ETFs now:

Diversification in the Tri-Polar World (US, China, Euro)

Most investors are heavily invested in U.S. Markets and should, instead, consider diversifying their portfolios globally. Though ADRs provide ease of entry, direct investment in local markets better reflects true market opportunities. By employing an investment strategy that not only distributes your capital across multiple US companies, but also across emerging opportunities around the world, you can balance your portfolio in a way that is nearly impossible to accomplish with U.S. equity investments, alone.

Global Exposure

Stock markets outside of the U.S. often move at a different pace than the U.S. market. This gives investors, who are already actively trading in the U.S. Stock Market, the comfort of knowing that a portion of their portfolio is less influenced by potential risks that primarily affect only U.S. Markets (e.g., U.S. Elections). Moreover, the sliding dollar bodes well for Non-U.S. investments. With an overseas investment, the continuing depreciation in U.S. currency implies an added benefit for U.S. investors who can potentially gain from overseas stock appreciation along with the currency benefit.

Expert Management

When investors place funds in a Non-U.S. ETF or Mutual Fund, they invest with experts who are experienced in buying and selling foreign stocks. This is important since buying stocks in foreign markets with foreign currency and local traders is often extremely difficult and expensive for individual investors to set up.

Accessibility

Non-U.S. Equity ETFs are accessible to all interested investors, with no minimum investment restrictions. The costs tend to be very low and usually amount to an annual cost of less than 75 cents for every $100 invested per year.

Performance

The performance for Non-US Equity ETFs has been rising since the Spring of 2020, along with other global markets. Though no one can promise future results, recent evidence suggests that the pendulum has already shifted—with Non-U.S. outperforming US stocks in recent weeks. This trend might very well continue for the foreseeable future.

Newcomers and seasoned investors alike can take advantage of the growth potential of blossoming, global businesses through Non-U.S. ETFs and Mutual Funds. Compared to other investment opportunities—bonds, real estate, gold, etc.— Non-U.S. Equities, especially Non-U.S. Small Cap funds, are well positioned to provide strong future growth.

Would you like to know where you can find the next Trillion $ growth stock? If so, ERShares may have an answer for you. It is an ETF with NYSE Ticker: ENTR. This ETF invests in the leading Entrepreneurial publicly listed companies around the world. ERShares was among the first to introduce a thematic approach to investing, having started 15 years ago following research conducted at Harvard University.

Our methodology is a proprietary trade secret, but the basic message is clear: ERShares selects the most entrepreneurial, strong growth, global companies and puts it to market in one easy-to-invest fund. Many investment companies claim Disruptive Technology, but only ERShares ensures that the right technology is matched with the right leaders. They believe that without the best entrepreneurial minds, technology alone will not get very far.

The ENTR ETF specializes in innovative HealthCare and Technology companies packed with All Star leaders including Elon Musk (Tesla), Jeff Bezos (Amazon), Reed Hastings (Square/Twitter), Jack Ma (Alibaba), Larry Page, Sergey Brin (Alphabet), Mark Zuckerberg (Facebook) and many others that are not yet as well-known but who will likely soon join that list.

ENTR is currently one of the strongest performing ETFs in its investment class and has an annual cost of 49 cents for every $100 investment. Moreover, the Fund Managers do not settle on prior performance and are constantly seeking exciting new growth stories in HealthCare and Technology to add to their ETF. The Markets have been strong for most of 2020, though frequently experience periods of volatility. Will this trend continue? Nobody really knows for sure or can offer promises about the future. However, ERShares team has confidence that whenever the next great growth story emerges, it will likely be led by a successful Entrepreneur, and probably reside within the ENTR ETF.